VA Loan Pros and Cons

If you’re an active-duty military member or Veteran considering a home purchase, you have one extra home loan option to weigh: a VA loan. VA mortgages are a type of home loan backed by the Department of Veterans Affairs, geared specifically to meet Veterans’ unique homebuying needs and challenges.

A VA loan is a great benefit for those eligible, but like any mortgage, it comes with pros and cons. Let’s explore the advantages and disadvantages of VA loans, whether they are a good option for different buyers, and if a VA home loan is right for you.

Many active military and Veterans choose VA loans because they offer advantages over other loans. Here are some of the benefits you can expect:

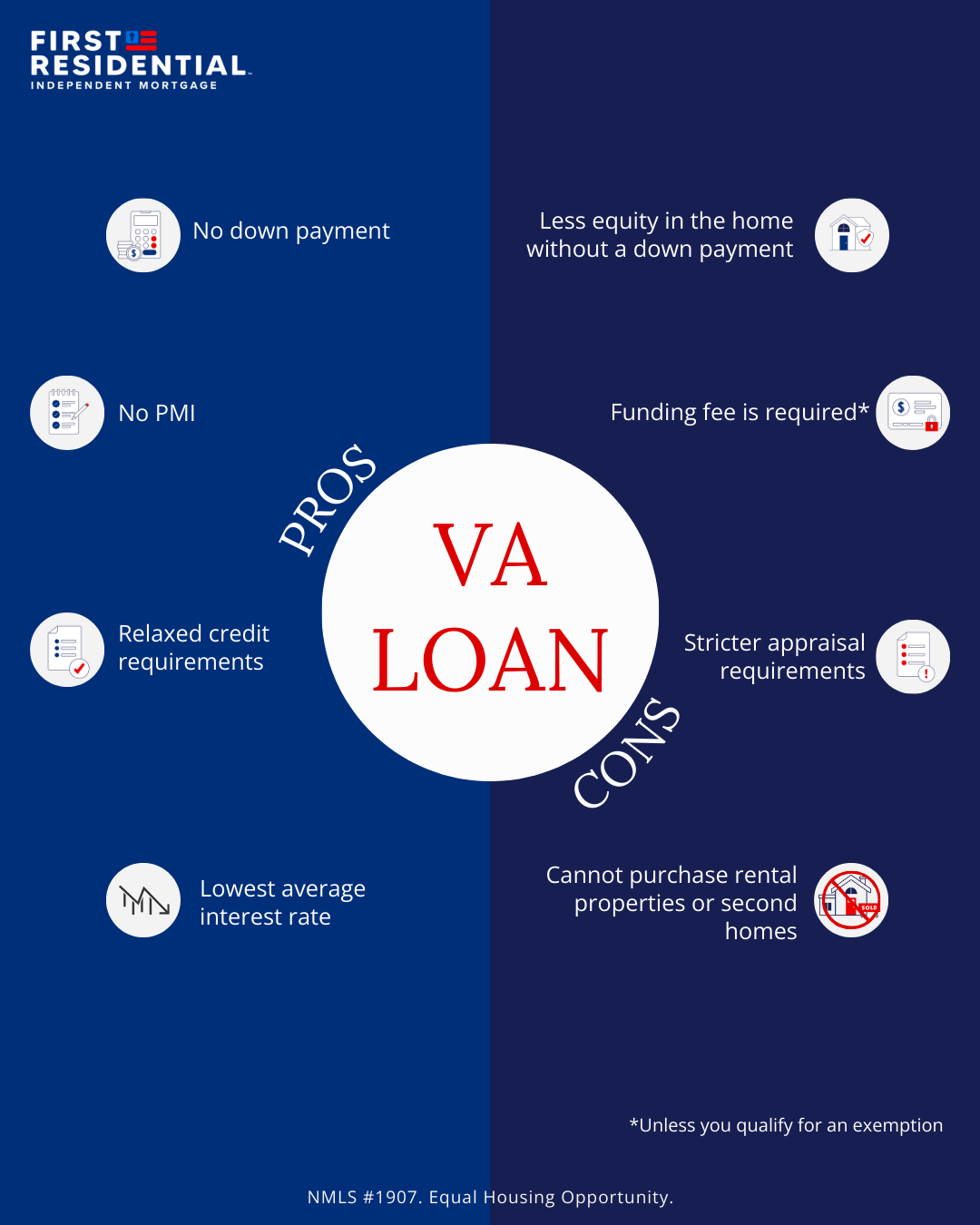

With a VA loan, you don’t have to pay a down payment. In fact, one of the main perks of a VA loan is the ability to fund your home purchase with $0 down.

If you want to use a conventional loan to buy your home, you typically need to put down at least 5% of the purchase price. In some cases, buyers might need to put down even more. Saving for a down payment can be especially tough if you’re deployed or on a fixed income.

Ready to see how much home you can afford with $0 down? Get a personalized VA loan estimate today.

Another benefit of a VA loan is that you won't have to pay private mortgage insurance (PMI). Conventional buyers typically need to pay for PMI if they put down less than 20% of the purchase price.

No PMI is a huge perk, as it can add a hundred dollars or more to your monthly mortgage payment each month. Removing that extra insurance from the monthly cost equation can help you qualify for a larger loan, too.

Connect with a First Residential loan expert at 1-800-906-8960.

A VA loan has relaxed credit requirements. Credit score minimums can vary by the lender and other factors, but VA loans have lower minimums than conventional loans. That can really come in handy for military members and younger Veterans, as it can be tough to focus on credit building while deployed overseas or on active duty.

VA loans also have shorter waiting periods after negative credit events, such as bankruptcy, foreclosure, and short sales.

VA loans’ low average interest rates are a significant money-saving benefit, and VA loans have historically had the lowest average fixed rates on 30-year mortgages. Lower rates help Veterans expand their buying power and potentially save thousands over the life of the loan. Rates vary based on the lender and other factors.

Certain types of mortgage loans can penalize buyers with extra fees for paying off their mortgage early. VA loans come with no prepayment penalties. That means you can pay off your mortgage early without having to worry about losing extra money in fees for doing so.

Another major perk of VA loans is that they’re assumable, meaning that when you sell a home purchased with a VA loan, the buyer has the option to take over the terms of the existing mortgage, whether they’re an eligible civilian or a service member. That’s a huge perk for buyers when weighing homes, and it can be a huge benefit to you when selling your home.

VA loans have two refinancing options: a VA Streamline refinance, also known as an Interest Rate Reduction Refinance Loan (IRRRL), which lets you easily refinance your mortgage to a lower rate with little paperwork, and a VA Cash-Out refinance, which lets you tap into your home’s equity to make repairs, pay off high-interest debt, or for any other purpose.

With the VA loan, you are exempt from both PMI and a down payment, which can save you money in the long run.

| Loan Type | Down Payment Required | PMI Requirement | Estimated Monthly PMI |

|---|---|---|---|

| Conventional Loan (average $388,000 loan) | 20% = $77,600 | Yes, if you contribute less than 20% down | 0.58-1.85% annual, $150-200/month |

| VA Loan (same $388,000 loan) | $0 | No | $0 |

Like any other loan type, VA loans also have potential disadvantages. These include:

One disadvantage of a VA loan is the additional cost of the VA funding fee. This fee goes directly to the VA and varies depending on the purchase and whether you’ve used this benefit before, ranging from 2.3% to 3.6%. Buyers can lower their funding fee by putting down at least 5%. Buyers can finance this cost into their loan. Veterans who receive compensation for a service-connected disability and select others are exempt from paying this fee.

VA loans are designed to help military members purchase homes for their primary residence — not for investment properties or vacation homes. Veterans need to intend to make their home their primary residence, typically within 60 days of closing.

The appraisal process for VA and FHA loans differs from conventional mortgages. Homes must meet the VA’s property condition requirements to ensure that Veterans purchase safe, sound, and sanitary homes. Any repairs that arise from the appraisal typically need to be completed before the loan can close. Sellers or even buyers can pay for those repairs to keep things moving.

While you have the option to buy a home without a down payment with a VA loan, there can be downsides to that, including a lack of equity. The more you pay into your home, the more equity — or the portion of the home you own outright — you have. Equity is one of the biggest perks of owning a home, but if you opt for a VA loan without a down payment, it can take a while to make enough payments to gain a substantial portion of ownership in your home.

As noted, VA purchase loans are only available for owner-occupied residences, which means that you don’t have the option of using your VA loan to purchase a rental property. However, VA buyers can purchase a multi-unit property – typically up to a four-plex – provided they intend to occupy one of the units.

Unsure if the funding fee or stricter appraisal rules will affect you? Start the application process to see what applies to you.

Whether or not a VA loan is worth it depends on your goals and specific situation. Several perks come with using this loan type, so if your goal is to own a home for you and your family to live in, a VA loan can help make that happen.

VA loans can be particularly beneficial for first-time buyers with lower credit scores, as they often require no down payment. On the other hand, another option might better suit those who can afford a large down payment, prefer not to pay the funding fee, or are looking for an investment property.

Every buyer’s situation differs. A trusted lender can help you run the numbers and evaluate all of your mortgage options.

Another factor to consider with a VA loan is whether you're eligible. Generally, you may be eligible if you have served:

VA loans can be a powerful tool to help you gain homeownership, but only if they align with your goals. To see if a VA loan might be right for you, talk to a First Residential loan expert.

Tyler Oswald is a Production Training Team Lead at First Residential, where she’s revamped training to make it more effective and engaging. With a strong background in FHA, Conventional, and USDA home loans, she’s all about equipping loan teams with the tools they need to succeed while keeping things collaborative and aligned with First Residential'se values.

More articles by Tyler Oswald