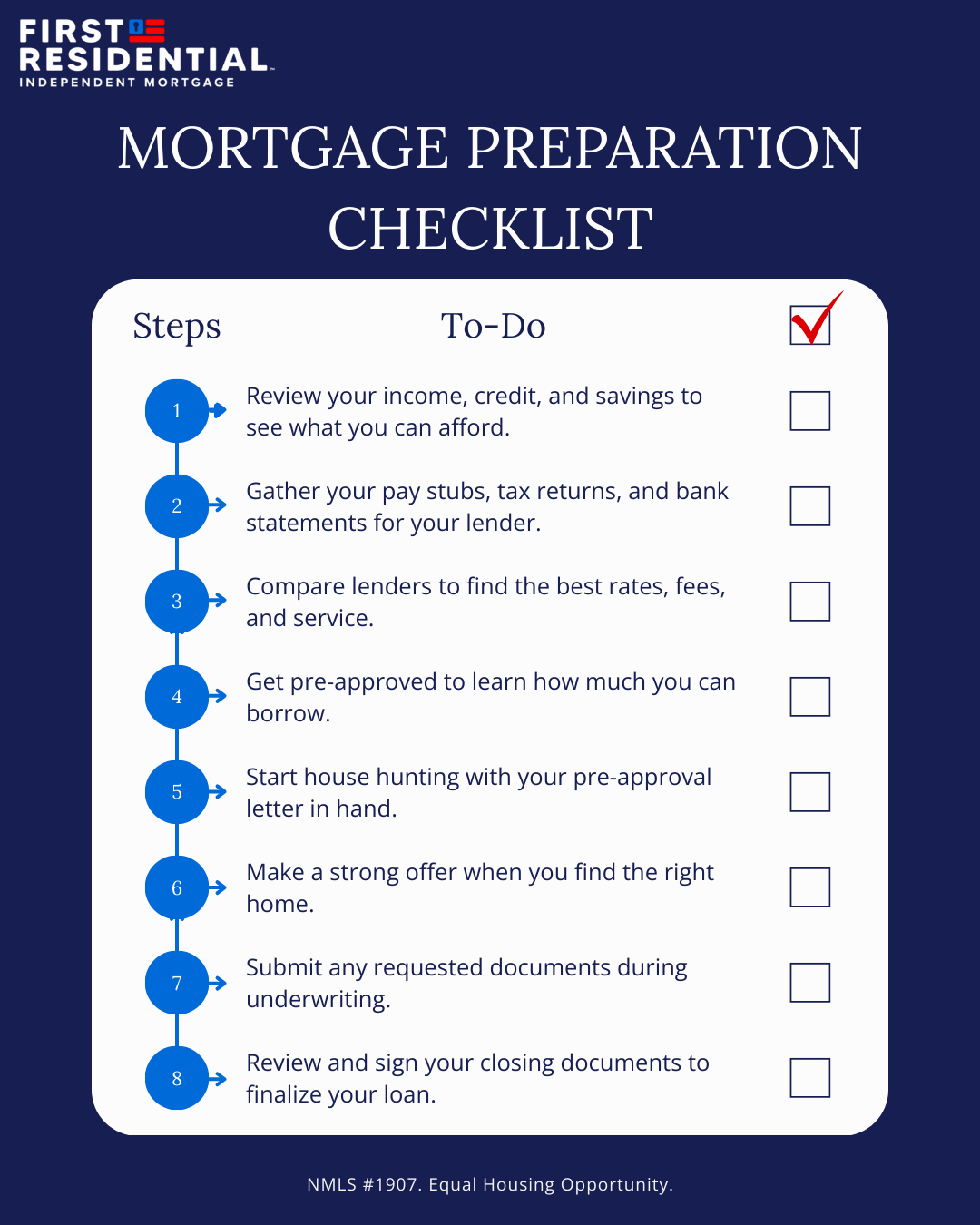

Mortgage Process Steps from Preparation to Closing

To help you transition from homebuyer to homeowner, here are eight steps to expect during the mortgage application process.

Let’s break down each step.

Prior to offering you a mortgage loan, any lender you work with will examine your finances to ensure that you can comfortably afford to pay back what you borrow. Lenders will also want to examine your finances to get a good idea of the right mortgage loan types for you. This typically includes an analysis of your income, credit, and assets. If you take an inventory of your finances before applying for a loan, you can identify any areas that might need improvement and maximize your chances of approval. This analysis should include:

Before applying for a mortgage, take a close look at your income and debts to determine how much you can afford to spend on a home. As a general rule, your housing costs should not exceed 28% of your gross income, and you should allocate no more than 36% toward monthly debt payments, which is known as the 28/36 rule.

Understanding how much of a mortgage payment your income can afford is a crucial step in the homebuying process. Knowing your housing budget before shopping can prevent the heartbreak of falling in love with a home out of your price range.

It’s a good idea to know your credit score before applying for a home loan. You can find your credit score with most major credit card companies through online banking or mobile apps. Regularly monitoring your credit helps you track your financial health and prepare for mortgage approval.

Your credit score can affect the loan options available to you. Typically, the better your credit score, the better the mortgage terms you will be offered. If your credit score is lower than average, lenders may perceive you as a higher risk, potentially limiting your loan options. On the other hand, if your credit score is excellent, you’ll have more mortgage options available — and probably lower interest rates.

You should also look closely at your liquid assets to determine your realistic buying power. These assets include the money in your bank accounts, retirement accounts, and even investments that can be quickly converted into cash. If your assets' values don't cover at least three months’ worth of bills, including your new mortgage payment, the home you’re considering may be a stretch.

You will need to provide your lender with a fair bit of paperwork during the loan process. For a faster experience, consider having the following on hand when applying.

Most lenders require you to provide at least two months’ worth of pay stubs as proof of income, though some may require more. Lenders may also ask you to provide your W-2s and tax returns from previous years. This helps the lender gain a better understanding of your financial situation.

If you’re self-employed or have other sources of income, you may need to provide 1099 forms, full tax returns, direct deposit statements, or other documents.

Your lender will pull your credit report as part of the loan process. To be proactive, you can request a copy of your credit report from each of the three major credit bureaus, which gives you the opportunity to check for errors and file disputes in advance. If your credit reports are frozen, make sure to temporarily unfreeze them before your lender pulls your credit. This helps avoid delays and prevents multiple pull attempts. If you have any missed payments or other credit issues, your lender may ask you for an explanation and what steps you are taking to prevent them from happening again.

Your lender will want to review your bank statements and other asset documents, such as investments or life insurance policies. You may also need to provide documents related to your liabilities, like current mortgage paperwork or your credit card statements.

When considering lenders, it is important to consider factors such as rates, fees, loan options, and customer service to determine the best fit for your needs.

Be aware that lenders may conduct a credit check during this process, which may temporarily affect your credit score. You can avoid having multiple pulls count against your credit by comparing different lenders around the same time. Multiple credit pulls within the same window count as a single credit inquiry, so don’t be afraid to apply with multiple lenders. Depending on the credit scoring model used, you will have between 14 and 45 days before additional credit inquiries count against you.

Check your mortgage eligibility!

After you’ve narrowed down your lenders, you can apply for mortgage preapproval, which requires your lender to take a comprehensive look at your finances.

If preapproved, your lender will issue a preapproval letter detailing the maximum amount you can borrow. You can also ask for more information on the interest rates you qualify for and other costs that could be associated with your loan.

With the preapproval letter in hand, you can begin shopping for a home. Your preapproval letter is important because it lets both agents and sellers know that you are a qualified and serious buyer.

When you find the perfect home, it’s crucial to submit the strongest offer possible, taking into account your location and the current market conditions. If your area has a competitive market, you may want to offer your highest purchase price upfront to avoid losing the home to other interested buyers. But don’t worry; if you’re using a real estate agent, they’ll be more than happy to help you craft a solid offer.

You can also talk to your agent about other contingencies to include, like a quick close or higher amounts of earnest money. In highly competitive markets, offering a higher earnest deposit or a fast closing may set you apart from other buyers.

After you have an accepted offer in hand, your loan will go through the underwriting process. During this process, your lender’s team will work to process your application and verify your financial information.

It’s normal for additional documents or paperwork to be requested during the underwriting process, so be sure to stay in touch with your lender and gather any necessary information. By answering promptly and thoroughly, you can expedite the underwriting process and reduce the chance of your loan falling through.

Your closing is the last step in the mortgage process. Before closing, you will be given a packet with your loan documents, known as the Closing Disclosure (CD). Review the documents in this packet carefully. It outlines the terms of your loan, including the payments and other costs you are responsible for.

At closing, you will sign all of your final loan documentation and pay any outstanding balances for your down payment, closing costs, or lender fees. Once these papers are signed and the money is paid, you can take possession of your new home.

The mortgage process can be intimidating for both new and repeat buyers, but preparing beforehand can definitely pay off. Take the time to gather your documents, do your research, and determine what loans and lenders are right for you. By putting in the work before you apply, you maximize your chances of a smooth process for both you and your lender.

Ready to start the process? Call 1-800-906-8960 to speak with a First Residential loan expert today.

The mortgage process typically takes 30 to 45 days from application to closing, but timelines vary depending on your lender, how quickly you can provide documentation, and the state of your finances. Staying organized can help speed up the process.

First Residential and many other lenders look for a minimum credit score of 620 for a conventional mortgage; however, some lenders allow lower scores. For FHA loans, First Residential requires a minimum credit score of 580 with a 3.5% down payment. A stronger credit score typically results in better loan terms and interest rates.

Underwriting typically takes between 2 and 14 days. During this process, your lender reviews your income, assets, debts, and credit history to confirm that you meet all necessary requirements. Providing documents quickly can shorten the approval process.

After approval, you will receive a Closing Disclosure with the loan terms and costs. Next comes closing, when you sign documents, pay remaining fees, and take ownership of your new home.

Dan Wasmer brings almost twenty years of experience in finance and banking. He is recognized for streamlining operations, strengthening collaboration, and finding creative solutions in complex, fast-paced loan scenarios.

More articles by Dan Wasmer