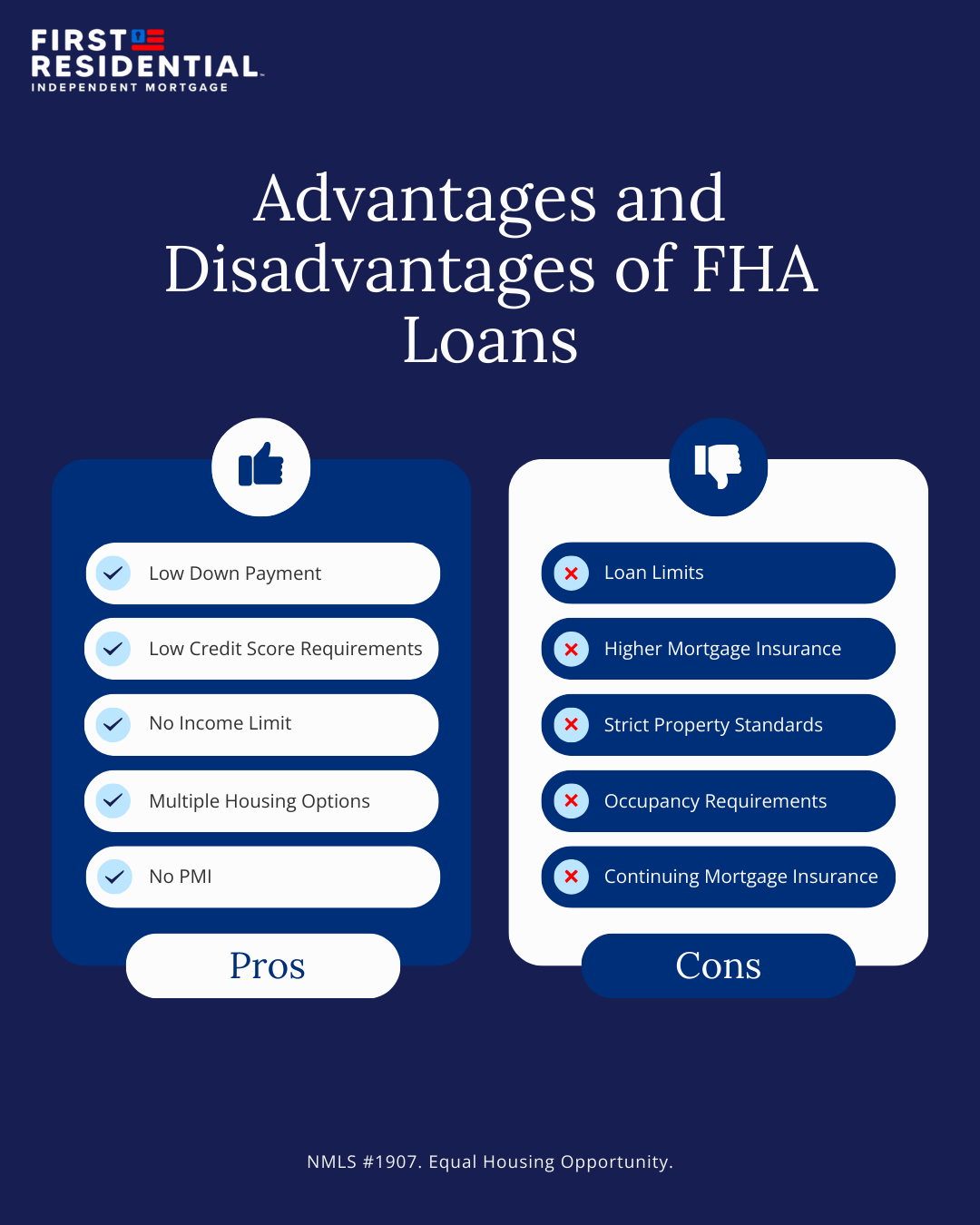

Pros and Cons of FHA Loans

FHA loans make homeownership more accessible with flexible credit requirements and a low 3.5% down payment option. Still, they come with higher long-term mortgage insurance costs, strict property standards, and borrowing limits that may not fit every buyer’s needs.

While FHA loans have many advantages, they may not be right for everyone. Before you make a major financial commitment, it's important to understand its pros and cons. Only then can you truly decide whether they're right for you.

An FHA loan is designed to help potential homebuyers with less-than-perfect finances buy a home. It offers many potential benefits that you may not be able to get when applying for a conventional mortgage. Here’s a closer look at some of the most important advantages of an FHA loan.

If you don’t want to wait forever to buy a home, the lower down payment requirement is one of the most significant FHA loan advantages. Most FHA loans allow you to put down as little as 3.5% of the purchase price. This is a huge advantage for buyers who don't have a large savings account or have limited financial resources. Other mortgage products may have down payments closer to the 20% mark.

Taking advantage of this opportunity can help you get into a home many years sooner than you could if you had to save up a larger amount.

Curious how much house you could afford? Check out our Affordability Calculator.

Many people with bumps in their credit history worry that they won't be able to qualify for a home loan. Luckily, FHA loans are available to borrowers with less-than-ideal credit.

Most lenders will write FHA-backed loans for borrowers with credit scores of 580 or higher. If you’re in the 500-579 range, don’t despair. It is still possible to qualify for an FHA loan, but you will need to come up with a 10% down payment instead of the standard 3.5%.

Note: While FHA technically allows scores as low as 500, most lenders set stricter standards and often look for 620 or higher. First Residential is currently looking for credit scores of 620 or above.

FHA loans are also sometimes a good option for people who have recently gone through a foreclosure or bankruptcy. Depending on your circumstances, you may be able to qualify for an FHA loan within one to two years after the incident.

FHA loans don’t have any minimum or maximum income requirements. Unlike USDA loans, which do impose income limits based on location and household size, FHA loans have no such restrictions. This means that higher-income earners with credit problems can still qualify for FHA loans. Even if you make a substantial salary yearly, you can still benefit from the lower down payment and relaxed approval requirements.

You can use an FHA loan to purchase multiple types of properties. This includes single-family homes, condominiums on permanent land, manufactured homes on permanent land, and multifamily homes with up to four units, though you may have difficulty finding a lender willing to do a manufactured loan. This is because manufactured homes often come with stricter appraisal requirements, higher perceived risk for lenders, and additional rules about the foundation and land ownership. As a result, fewer lenders are willing to offer these types of FHA loans.

This variety still gives you plenty of options and some room to get creative. For example, as long as you live there, you could buy a multifamily home and use the rent you would charge on the other units to qualify for the loan.

If you put less than a 20% down payment, most conventional loans require you to carry private mortgage insurance (PMI). This insurance protects the lender if you fail to repay your loan. The premiums for PMI are often much higher if you have bad credit. With an FHA loan, however, you’ll pay the same insurance premium regardless of your credit score. If you’re credit-challenged, this could save you a significant amount of money over the lifetime of your loan.

While FHA loans certainly offer many advantages, there are also some potential drawbacks you need to be aware of. Researching some common problems with FHA loans will help ensure you don’t encounter any surprises during your homebuying journey.

If you’ve got your eye on a high-priced home, FHA loan borrowing limits could be one of the biggest FHA loan cons. The limits vary depending on the county where the home is located. This allows them to account for the difference in property from one area to the next.

In 2026, the borrowing limits for FHA-backed loans for a single-family home range from $541,287 to $1,249,125. These limits adjust periodically based on a percentage of the current standard limits for conventional loans. If you’re using an FHA loan to purchase a multifamily home, these limits are higher and vary based on the number of units in the home.

Does your dream home fit FHA guidelines? Take a look at the FHA loan limits today.

While borrowers using FHA loans with a down payment of more than 20% don’t have to pay private mortgage insurance (PMI), they are required to pay for a different type of mortgage insurance. This is divided into two parts. First, you’ll need to pay a mandatory upfront premium of 1.75% of the loan amount.

In addition, an annual mortgage insurance premium (MIP) is added to your monthly payments. For most buyers, this annual premium is 0.55% of the loan balance.

For example, if you take out a $250,000 FHA loan, the upfront premium would be $4,375, which can often be rolled into the loan. The annual MIP would be about $1,375, adding roughly $115 per month to your mortgage payment.

To put this in perspective, PMI on a conventional loan typically ranges from about 0.2% to 1.5% per year, depending on your credit score and down payment. Because FHA’s MIP rate is fixed and not credit-based, borrowers with strong credit may find that FHA’s insurance costs run higher overall than what they might pay with PMI on a conventional loan.

The government requires that all properties purchased with FHA-backed loans meet minimum health and safety standards. If the property you’re considering isn’t structurally sound or has safety issues, you may not qualify for an FHA loan. If you're considering buying a major fixer-upper, this could be an issue.

Somebody must inspect the property before you can qualify for the loan. Some things that could cause it to fail include a sagging foundation, a leaking roof, signs of decay, faulty wiring, or contaminated soil. If the inspection uncovers any of these issues, they must be fixed before your loan is approved.

You can only use an FHA loan to purchase your primary residence. If you’re planning to buy an investment property or a vacation home, you’ll need to use a different type of loan.

If you put down less than 10% of the home’s purchase price, an FHA loan requires you to carry mortgage insurance for the loan's lifetime.

This differs from conventional loans, which allow you to drop your mortgage insurance once you have at least 20% equity in your home. Even if you put down 10%, you must carry the insurance for 11 years. This mortgage insurance requirement may increase your overall cost compared to insurance premiums on other types of mortgages.

Carefully weighing the pros and cons of FHA loans is an important step in deciding whether it’s right for you. If you’re unsure, the professionals at First Residential are here to help. We’ll provide you with expert advice about FHA loans and help you choose the best option for your needs.

Ready to take the first step? Get your personalized quote now.

Crystal has experience in many parts of the homebuying process, from closing to title work. As someone who has bought multiple homes across state lines, Crystal also pulls on her personal experience when helping buyers through the process.

More articles by Crystal Shifflett